Weekly Manhattan and Brooklyn Market Update: 11/10

Real Estate Elegan November 8, 2025

Real Estate Elegan November 8, 2025

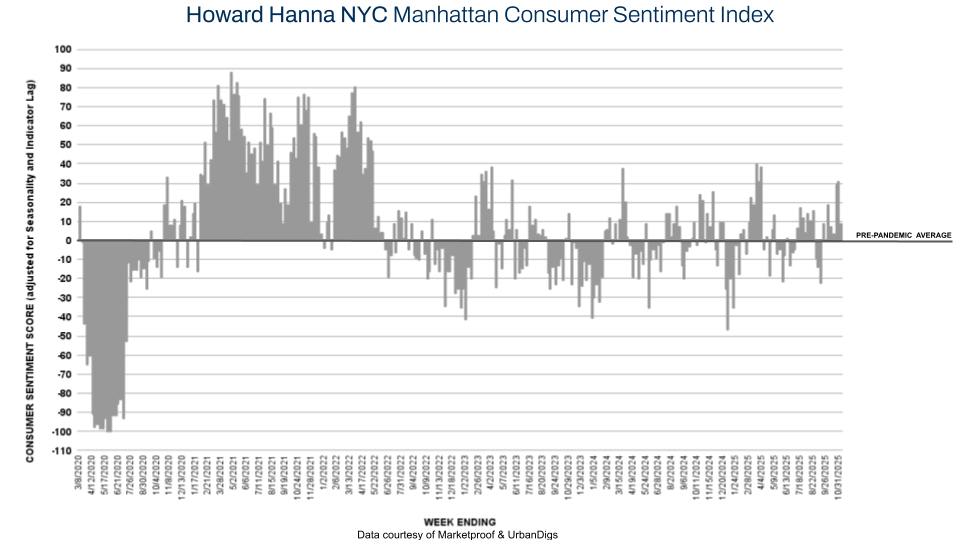

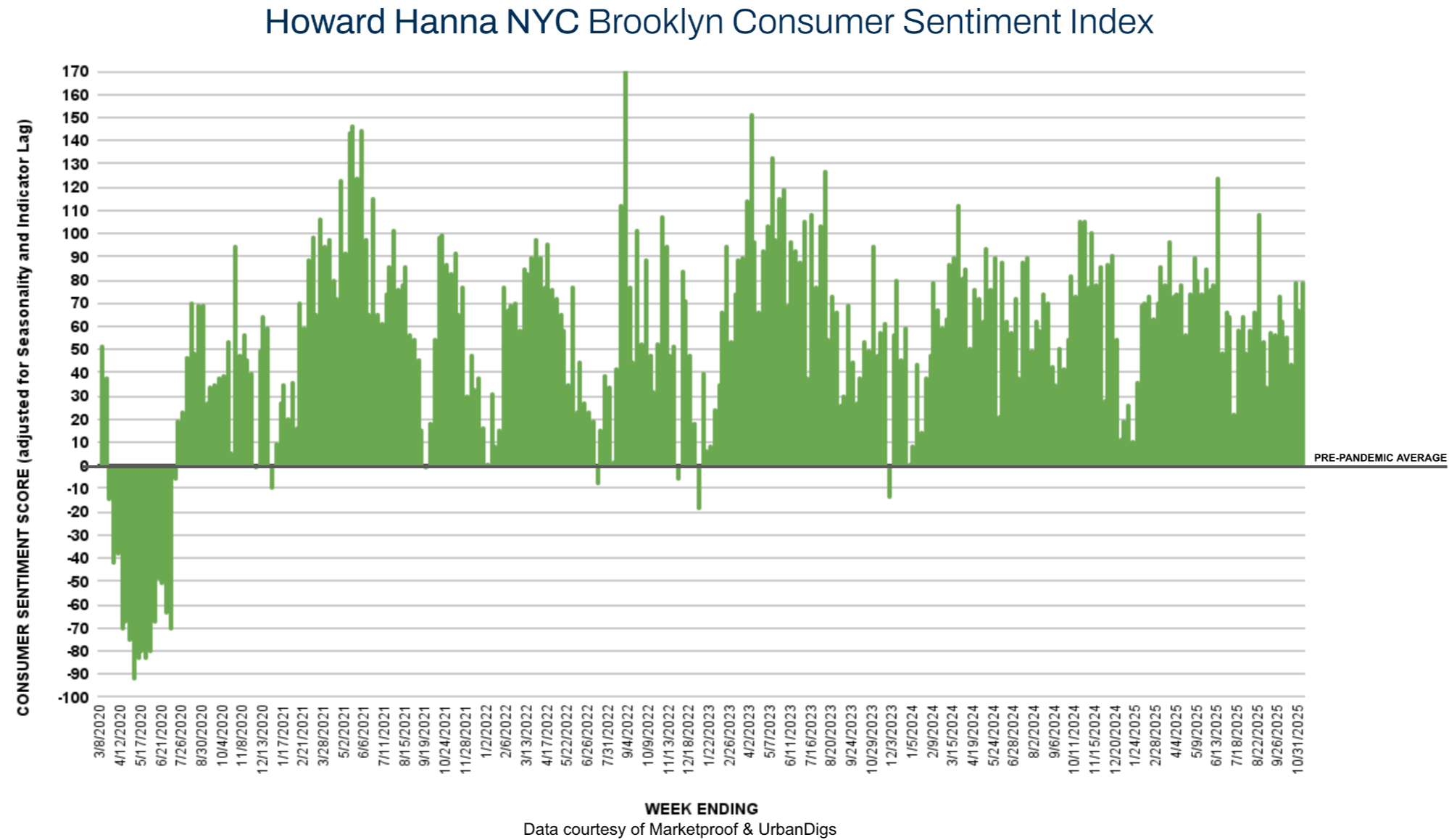

The New York City market is easing into its late-fall phase. Manhattan’s inventory is trending down after a strong October, while Brooklyn’s supply begins to stabilize. The Howard Hanna NYC Consumer Sentiment Index slipped from 40% to 24%, underscoring both seasonal caution and political recalibration following Mayor-elect Zohran Mamdani’s unexpected victory.

While uncertainty often follows new leadership, early signals from the Mamdani transition suggest a pragmatic stance toward property owners and housing supply — potentially softening concerns about anti-development rhetoric. Nevertheless, the market remains structurally sound. Contract volume continues to outperform last year’s lows, and buyer engagement remains steady in the sub-$2M category.

Mamdani’s win is reshaping expectations across the real estate sector.

Despite campaign trail tension, his support for ballot proposals 2–5, all of which passed, indicates a more development-friendly posture than headlines imply. His appointments — notably Maria Torres-Springer, a seasoned former Deputy Mayor — are being viewed as a stabilizing influence.

Industry leaders from Hudson Companies and SPONY (Small Property Owners of New York) report early discussions focused on property tax reform and small landlord relief, not punitive regulation.

In short: the narrative may be shifting from confrontation to collaboration — though the proof will come in 2026 policy outcomes.

Manhattan’s inventory fell to 6,641 homes (–2.9% WoW, –0.7% YoY) as sellers began their pre-holiday pause. New listings dropped to 225 units (–21% WoW, –15% YoY), confirming the start of the annual winter contraction. This tightening is healthy: it prevents oversupply and keeps pricing steady even as transaction velocity slows.

Brooklyn’s supply declined to 3,551 homes (–2.3% WoW, +7.6% YoY), its first contraction after a month of growth. New listings fell to 139 units (–24% WoW, –20% YoY) as more sellers exit the market early for the season. Still, YoY inventory growth remains positive, offering buyers a wider selection than last fall — especially in mid-range price bands where demand remains durable.

Pending activity remains resilient, reflecting deals initiated during October’s brief surge now moving toward close.

Contracts signed fell to 212 (–17% WoW, –5% YoY), sending the Howard Hanna NYC Manhattan Consumer Sentiment Index down from +31% to +9%.

This aligns with historic seasonality — Manhattan’s November contract pace typically dips 10–20% versus mid-fall levels as buyers and sellers shift focus to year-end planning.

Brooklyn recorded 138 signed contracts (+8.7% week over week, –10% year over year), lifting buyer sentiment from 67% to 79%. This late-season uptick could mark one of the borough’s last bursts of 2025 activity before the typical Thanksgiving slowdown. Overall, residential sales remain below last year’s pace.

Marketproof tracked 29 new development contracts across 23 buildings. Top performers included:

212 West 72nd St (Lincoln Square), One Manhattan Square (Two Bridges), and The Florian (Gramercy Park) each signed 2 contracts.

Her experience, expertise, and engaging personality make Sonal the perfect combination of advisor, advocate, and strategist. She is the proud owner of several NYC properties and a skilled negotiator with a deep understanding of people and sharp instincts about market trends.